Strategy and Business

Sustainability led strategy

Strategic priorities

Our four strategic priorities for 2022 – 2026 will help guide the Company’s strategic direction towards becoming the green partner for deep sea shipping. Our strategic priorities serve as a guide to ensure we are focusing our resources and efforts on what is most important to drive long-term success.

Customer centric

Deliver shipping services that create customer satisfaction and loyalty

Building strong customer relationships is at the core of our strategy and critical for long term success. We engage closely with our core customers to build commercial resilience, strengthen our contract backlog, and continuously evolve our service in response to the changing needs and priorities of our customers.

Greener

Become the greener deep-sea operator to secure our future

We are investing in green fleet renewal to facilitate low carbon transportation and provide our customers with green optionality to achieve their decarbonization goals. Additionally, we take an active stance in the public arena, collaborating with the industry and relevant stakeholders to advocate for common standards and a greener future.

Highly efficient

Reduce voyage costs and maintain lean operating model to reduce unit costs

Operational efficiency is key to delivering a competitive product to our customers. We continuously look for opportunities to reduce voyage costs and maintain a lean operating model across all areas — from optimizing our global trade network to streamlining internal processes.

Digitally enabled

Leverage digital tools to improve customer experience and operational efficiency

We are actively embracing advances within big data processing, computing power, cloud technology and AI. These are enabling digital transformation of our core processes in customer interactions, voyage management as well as cargo and vessel operations

Corporate purpose

Planet

Sailing for sustainability

Corporate purpose

As a shipping company operating worldwide, we need to take responsibility for the environment we operate in, and sustainability has been and is at the core of our operations. We have a solid history of emission cuts and long-term efforts to combat climate change, and are on a clear path towards a zero emissions future.

Our strategy has been shaped to best meet our commitments and continue to help decarbonize our customers supply chains. We will cut carbon emissions by more than 30% by 2030 compared to 2019. Our comprehensive newbuild program with the Aurora Class vessels, is designed for a greener future and the vessels are the first PCTCs to receive DNV’s ammonia and methanol-ready notations. Read more about our sustainability ambitions and targets in the Sustainability Statements.

Development goals

-

Cut carbon emissions by more than 30% from 2019 to 2030* and reach net zero by 2040

-

Partner with customers to create and grow the world’s greenest deep-sea shipping services

-

Raise the bar of asset life cycle mgmt. based on our responsible business philosophy

* The decarbonisation target refers to a more than 30% reduction in the Group’s fleet efficiency measured by the capacity gross ton distance (cgDIST) by 2030 compared to 2019 (the “30 by 30 Target”). For more details on our net zero ambitions, please refer to E1-1 in the Sustainability Statements.

Empowering people to be their best

Corporate purpose

As a global operating organisation, we are committed to provide a safe and healthy workplace, creating an open and inclusive culture, and a working environment in accordance with our company values. We promote the wellbeing of our people and local communities through relevant programmes and offers. We cultivate and invest in diverse agile teams who learn together, collaborate globally and drive bold transformation for our business, partners and customers.

We adopt digital tools to continually develop our shipping heritage and support efficient and safe operations.

For more details on people and social aspects, see social information in the Sustainability Statements.

Development goals

-

Cultivate and invest in diverse agile teams who learn together, collaborate globally and drive bold transformation for our business, partners and customers

-

Promote the wellbeing of our people and local communities through relevant programs and offers

-

Adopt digital tools to continually develop our shipping heritage and support efficient and safe operations

Prosperity

Growing responsible business

Corporate purpose

Höegh Autoliners is committed to deliver the best service to its customers and stakeholders, while ensuring compliance with ethical business principles, applicable laws, and environmental and community norms. We have a focus on developing lasting relationships with customers sharing our business philosophy.

A key component of our compliance program is customer privacy, including the European General Data Protection Regulation (GDPR).

We optimise network and capacity to maximise available capacity while maintaining safe operations, and ensure financial resilience by management of financial leverage and risks. We are committed to sustaining the profitability of our operations and generating long-term value for our shareholders, in addition to promote prosperity for the planet and society. The strategy is centred around continuous relationships, which we belive is essential when building resilience for the future. Our ambition is to act responsibly and with integrity in all tax matters, ensuring full compliance in every jurisdiction across the world.

Development goals

-

Develop lasting relationships with customers sharing our business philosophy

-

Ensure financial resilience by management of financial leverage and risks

-

Optimise network and capacity to maximise available capacity while maintaining safe operations

Business model at a glance

Long-standing pure-play RoRo liner business, serving longstanding contract customers and spot commitments(1) via vessels deployed in major deep sea trade routes.

Fully integrated global organization with in-house commercial- and operational management and technical service.

Top 6 largest RoRo shipowner with the world’s greenest fleet of PCTCs – outperforming segment carbon intensity average by 10%.

Transformational green newbuilding program with superior efficiency.

(1)Spot commitments defined as rate agreements and other cargo commitments with contract duration of up to 1 year.

Selected customers

Cargo segments

-

Factory New Light Vehicles

With our commitment to innovation and customer satisfaction, Höegh Autoliners has established a leading position in the automotive transport industry. Car manufacturers worldwide transport their brand-new vehicles on RoRo shipping vessels. These vessels function like mobile parking structures, ensuring the secure anchoring of cars to their decks.

-

Previously Owned Vehicles

Our global network of deep sea trades positions us as a reliable partner for both global car manufacturers and shippers of used vehicles.

-

High & Heavy

Our vessels and specialized equipment ensure out-of-gauge cargo’s safe and efficient transportation. Our extensive rolltrailer fleet incorporates a wide range of cargo-carrying equipment, ensuring that we can accommodate diverse cargo sizes.

-

Breakbulk

At Höegh Autoliners, we are committed to providing exceptional services for the transportation of various types of cargo, including breakbulk and other out-of-gauge shipments. To cater to the unique requirements of such cargo, we rely on our modern and specialized rolltrailers. Breakbulk include mining equipment, rail equipment and construction machines.

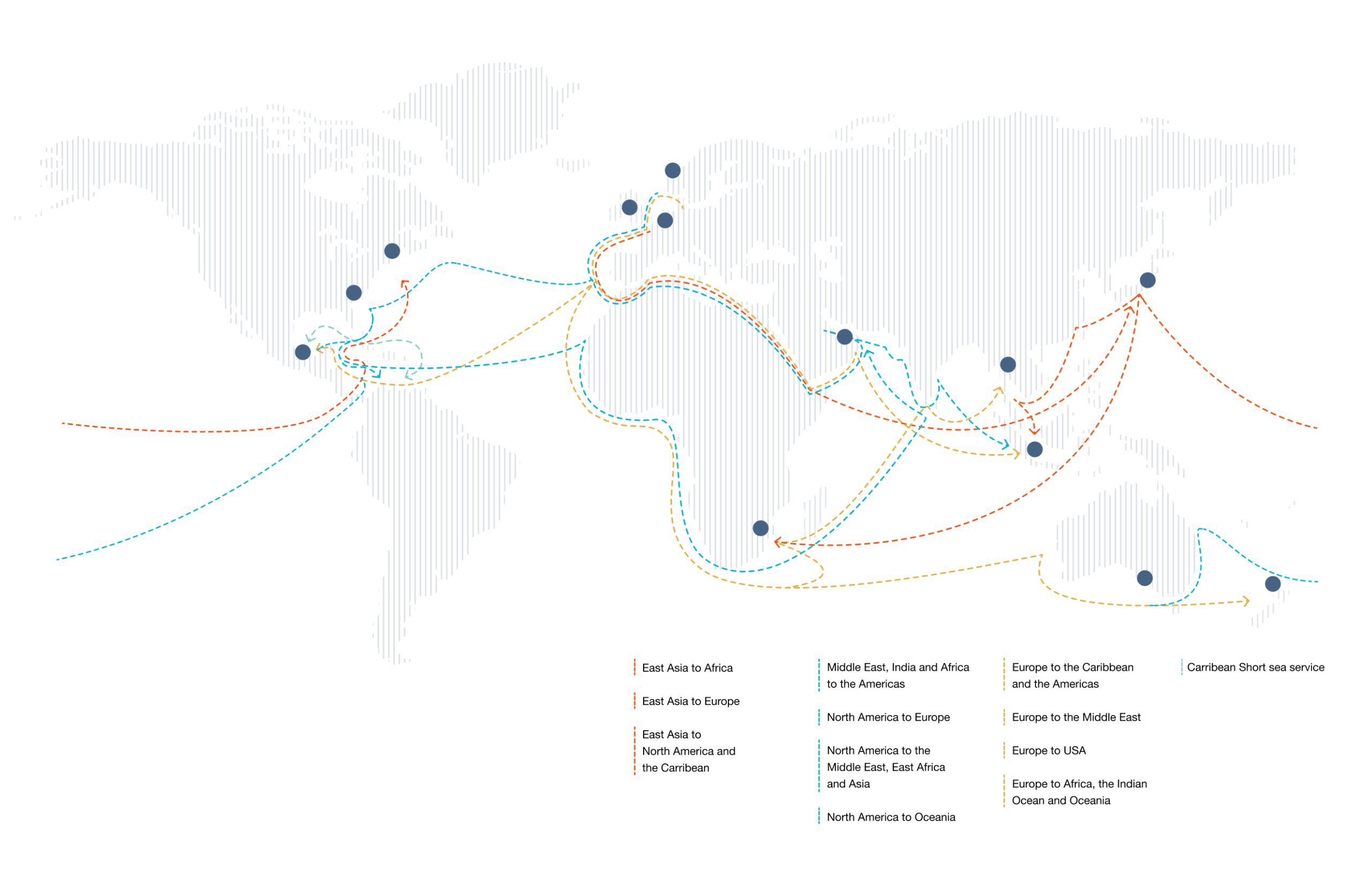

Global network and organisation with focus on operational efficiencies

Overview of trade routes

Market developments

The global economy grew by an estimated 2.7% in 2024. The outlook for 2025 is influenced by potential U.S. policy shifts and their domestic and international implications, with export-sensitive economies having greater exposure.

For global car carrier shipping, the year was defined by continuous strong growth of exports from China, including a 40% share of NEVs, U.S. and EU import tariffs on Chinese EVs and the de facto closure of Red Sea transit forcing major carriers to re-route vessels via Cape.

Continued recovery in global auto demand

and deep sea shipments

The demand for global light vehicle demand continued its post pandemic recovery in 2024, albeit at a slowing pace. Global vehicle sales are provisionally estimated at 88.3 million units, marking a 1.7% increase on 2023. The growth in auto demand was driven by normalization of global automotive supply chains and return to a more traditional demand-driven model. Compared the pre-COVID-2019 performance, the 2024 sales volume was still down 1.8%.

Global sales overview 2024

2024 Global auto sales reached 88.3 million units, up by 1.7% from 2023. The demand for global light vehicle demand continued its post pandemic recovery in 2024, albeit at a slowing pace. The growth in auto demand was driven by normalization of global automotive supply chains and return to a more traditional demand-driven model. Compared the pre-COVID-2019 performance, the 2024 sales volume was still down 1.8%.

In 2024, vehicle sales in Höegh Autoliners’ relevant destination markets were up 2% – marginally higher than the overall global sales growth. Vehicle electrification and EV industrial policies in Europe were a key driver behind strong European sales growth. Light vehicle demand in North America also continued to improve against previous year levels.

The outlook for global vehicle sales in 2025 is somewhat uncertain. The light vehicle demand recovery in the U.S. may lose some momentum due to the new U.S. Administration introducing new tariffs and trade policies. However, our current estimate is for global sales to improve by 1.7% reflecting a mix of both opportunities and threats. Consumer demand could remain challenged by affordability issues, including higher interest rates and energy prices.

Vehicle shipments

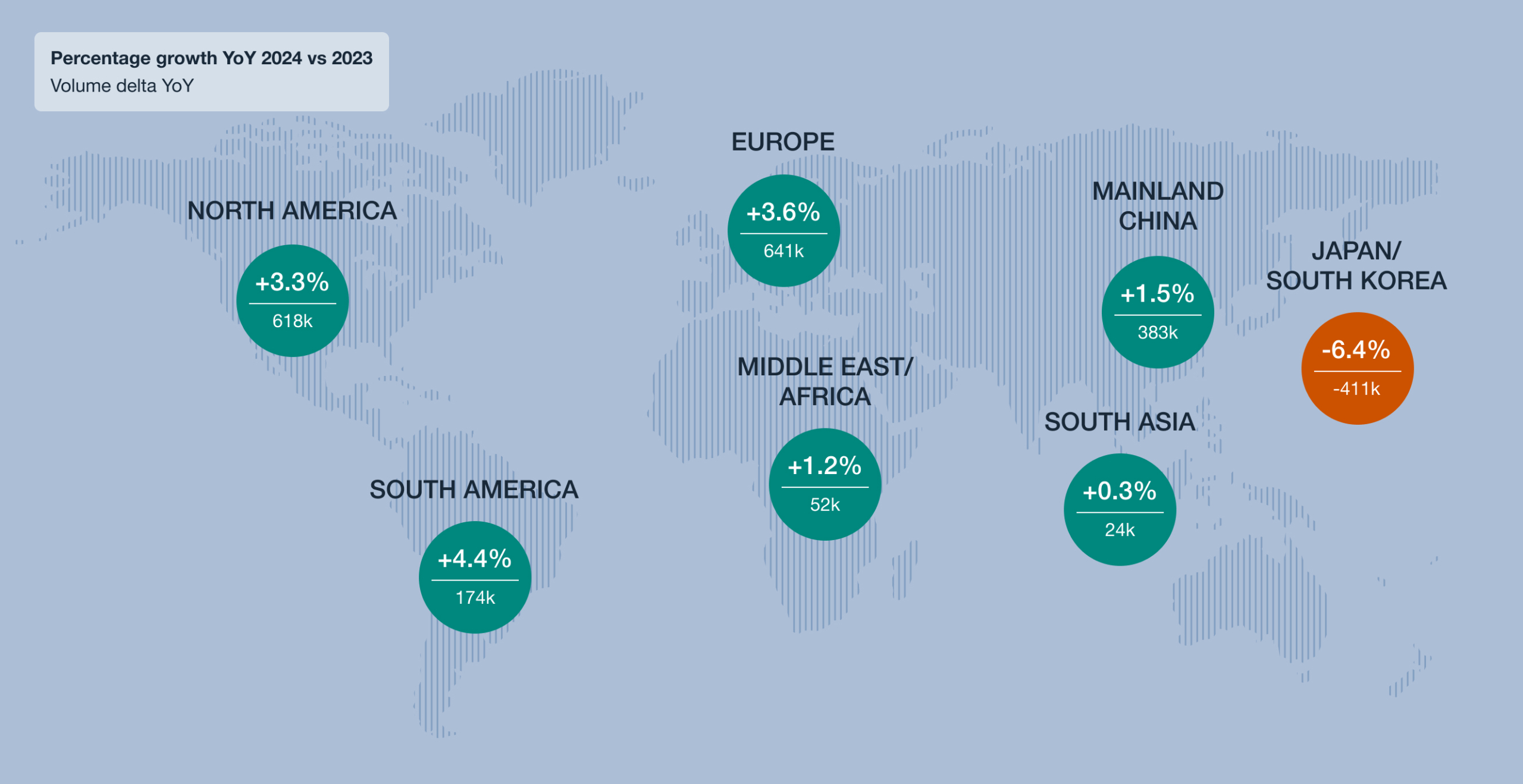

Total light vehicle shipments in Höegh Autoliners’ relevant deep sea trade lanes increased by an estimated 9% in 2024 – a result of a solid, supply-unconstrained sales growth across all markets. Asia further increased its role as the most important sourcing region of vehicle exports. Total light vehicle exports from Asia expanded by 7% in 2024, driven by strong Chinese shipments (up 21% y-o-y).

China continued to cement its position as the largest vehicle exporting country by volume with 2024 total exports of 5.9 million units (incl. overland and shortsea volumes), compared to 4.2 million units exported from Japan.

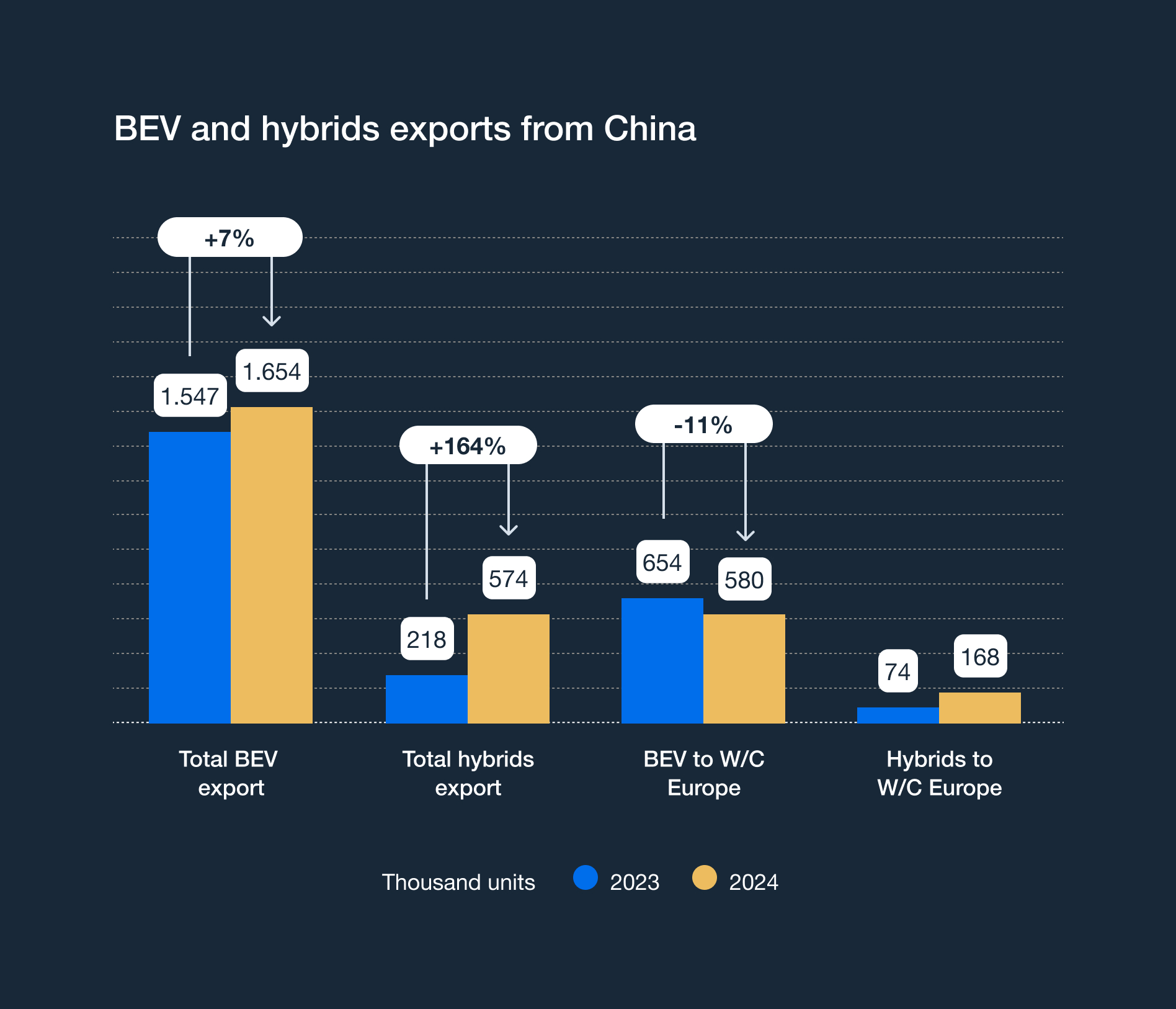

China’s 2024 BEV exports to Western and Central Europe declined by 11% y-o-y as a direct result of EU’s import tariffs on Chinese electric cars in 2H 2024. However, this decline was more than offset by growth in Chinese exports of hybrid vehicles – up by 127% in 2024 with most of this growth taking place in Q4.

Japan’s vehicle exports contracted by 5% in 2024, with shipments to Europe down 14% and shipments to the US down 8%. In the same period, S. Korean vehicle shipments were up a modest 1% (with 10% growth to U.S. largely offset by a 10% decline to Europe).

High & Heavy (HH) sales and shipments

2024 was a year of readjustment for the global construction equipment market, which had seen strong sales during the pandemic years. Higher interest rates have dampened global construction and resulted in an estimated 11% fall in global equipment sales (in value terms). The outlook for 2025 is somewhat flat with an expected pick up from 2026.

After enjoying several consecutive years of record equipment sales, the N. American market is estimated to have declined by 10% in 2024 as demand cooled due to higher interest rates and uncertainty ahead of the presidential election with buyers holding off on purchasing until the policy agenda for the next four years is clearer. However, 2024 was still the third best year in history in terms of machines sold. 2025 will likely see a renewed activity with new Administration supporting domestic construction.

The Eurozone construction sector remained in decline at the end of 2024. Interest rates and the residential construction market were key factors negatively affecting the mini excavators and compact equipment segments (shipped mainly in containers). The demand for larger equipment (shipped mainly by roro) remained steady. Total equipment sales are expected to be flat to positive in 2025.

2024 global deep sea shipments of core H&H equipment reflected moderating, mixed demand recovery, contracting 1% y-o-y. Asia’s core construction equipment shipments (all sizes) in deep sea trades were flat on 2023, but nevertheless 103% higher when compared to the same period in 2019 as China’s deep sea shipments tripled between 2019 and 2024. China dominated deep sea shipments from Asia in 2024 (61% of total exported volume). The continuous Chinese export expansion was partly driven by weak domestic market and excess domestic production capacity. Shipments from Asia to USA, a key market for Höegh Autoliners, were up 14%.

Global PCTC fleet

The global PCTC fleet trading in the deep-sea trades totalled 724 vessels (4.3 million CEU capacity) by 4 March 2025. No vessels were recycled in 2024. The global order book counted 200 vessels, of which 57 vessels are scheduled for delivery in 2025, 58 vessels in 2026, 47 vessels in 2027, 38 vessels in 2028-2031. The capacity on order is equal to 37% of the total fleet.

Page footnotes

Market developments in this section relate to Höegh Autoliners key destination markets: Western/Central Europe, North America, Middle East, Oceania

Sources: GDP forecasts, FNLV sales and shipment forecast data is based on the latest available S&P IHS sales and production forecasts (Jan/Feb 2025).

H&H shipment data is based on customs statistics extracted from S&P Global Trade Atlas.

PCTC fleet data is based on Clarksons Platou data 4 March 2025 (vessels over 2 000 CEU capacity).